The newly enacted Tax Cuts and Jobs Act of 2017 is the most significant income tax overhaul since the Ronald Reagan presidency. This article is the second in a two-part series on tax reform. While the first article in this series focused on the income tax law pertaining to businesses, this article will focus on the changes made to individual income tax laws.

The newly enacted Tax Cuts and Jobs Act of 2017 is the most significant income tax overhaul since the Ronald Reagan presidency. This article is the second in a two-part series on tax reform. While the first article in this series focused on the income tax law pertaining to businesses, this article will focus on the changes made to individual income tax laws.

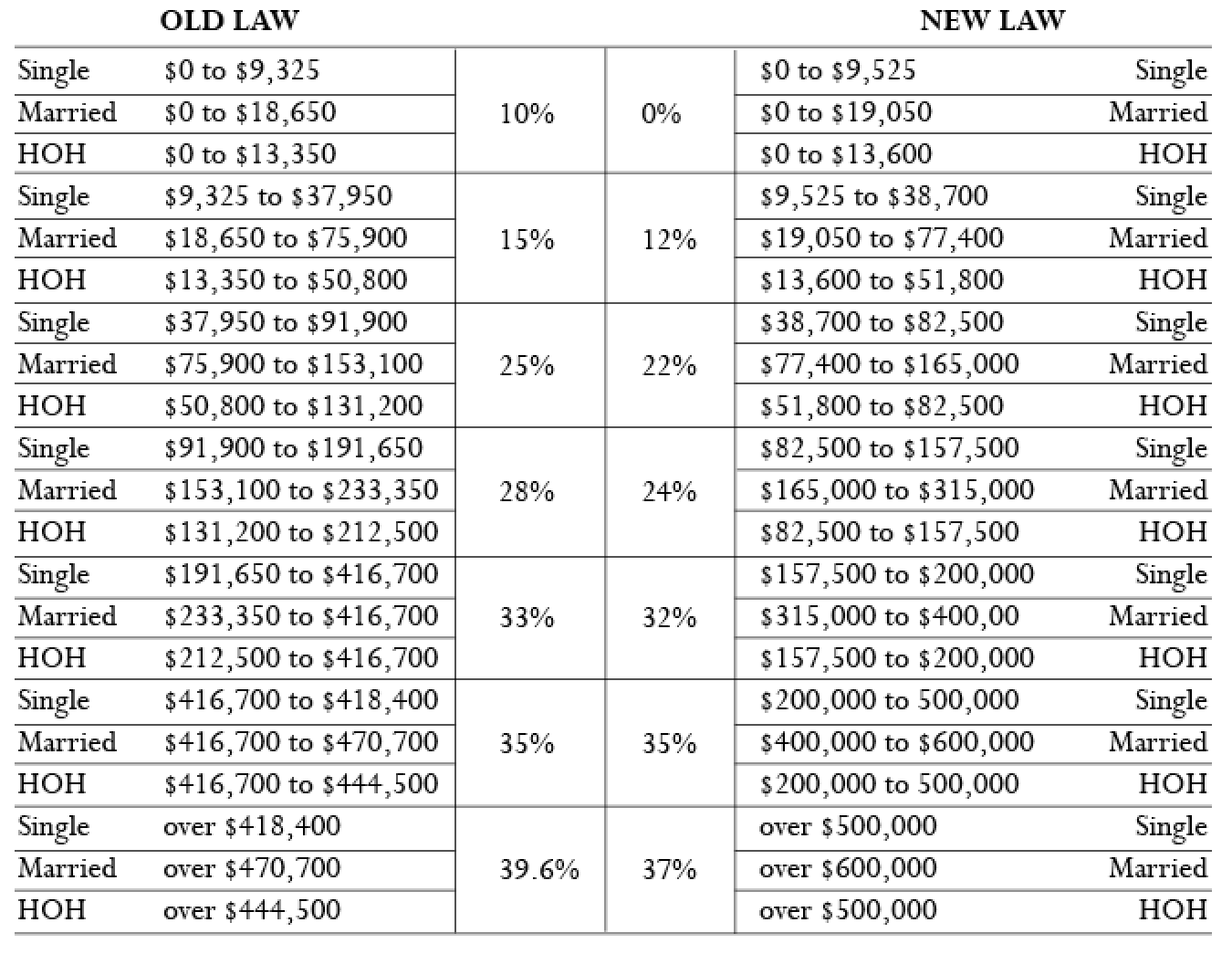

The keystone aspects of the new law are the new lower personal income tax rates and expanded income tax bands. Below is a table comparing the old law to the new law:

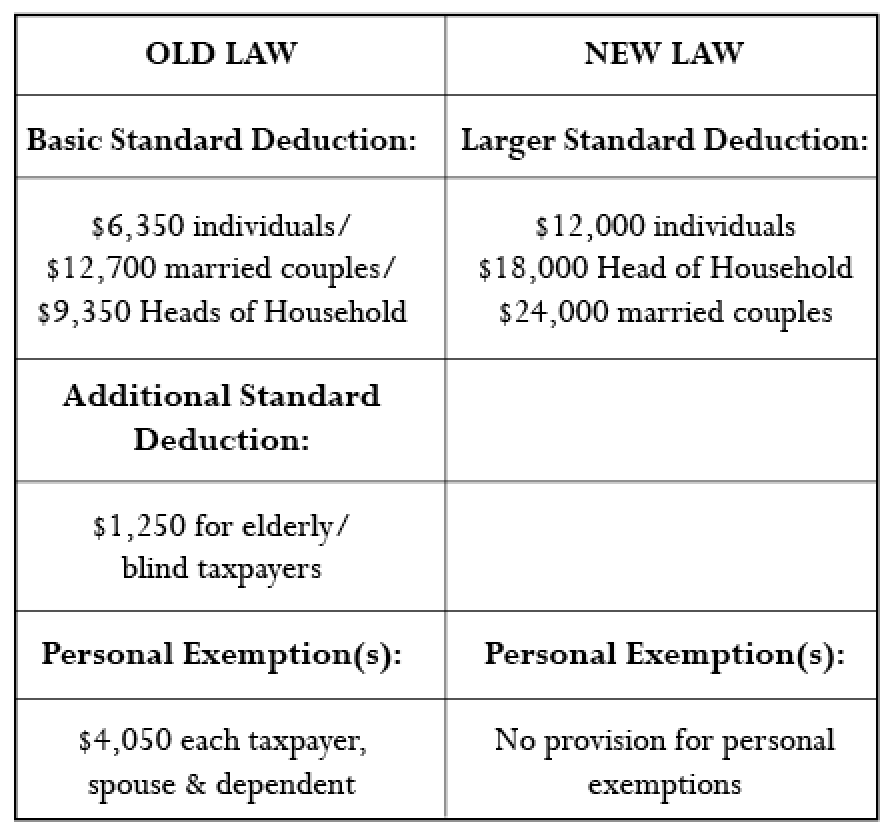

Just as importantly, there were major modifications to the way taxable income is computed. The following table illustrates the changes in the law which occurs when computing taxable income from adjusted gross income:

Since personal exemptions have been eliminated and tax rates have been reduced, individuals who are wage earners, are encouraged to review and, if necessary, file a new Federal withholding certificate (Federal form W-4) with their employers. It may mean a larger paycheck! If you are unsure what to do, the Internal Revenue Service has on online calculator to assist taxpayers with these selections. You may find this calculator at https://apps.irs.gov/app/witholdingcalculator/ Otherwise, please contact your tax professional.

The next most significant change to occur in computing individual income taxes are the types and amounts of itemized deductions now allowable by law. These are most commonly found on Federal Form Schedule A-Itemized Deductions. The following is a presentation of the changes in the order in which they appear on the form:

Medical deductions: Qualified medical expenses are currently deductible in excess of 7.5% of Adjusted Gross Income. This will remain in effect for 2017 and 2018. In 2019, the qualified medical expense threshold will rise to 10%.

State & local income taxes/real estate taxes: The deductible amount of state, local and real estate taxes will be capped at ten thousand dollars in 2018.

Mortgage interest: The new law modifies the amount of mortgage interest that is deductible. It imposes a lower dollar limit on mortgages that qualify for the home mortgage interest deduction. Beginning in 2018, taxpayers may only deduct interest on $750,000 of qualified residence loans ($375,000 married filing separately). While the law eliminates the deduction of interest from proceeds of a Home Equity Line of Credit (HELOC), the Internal Revenue Service has provided additional guidance in IR-2018-32, and they will continue to allow the deduction of HELOC interest. In the event a taxpayer has mortgage interest from a loan greater than the current $750,000 limit, please consult IRS Publication 936-Home Mortgage Interest Deduction or call your tax professional. Lastly, the investment interest deduction has been limited to investment income.

Charitable Contributions: The new law increases the adjusted gross income limitation for cash charitable contributions made by individuals to public charities and certain private foundations from 50% to 60%.

Casualty/Theft losses: Under the old law, a deduction may be claimed for any loss sustained during the tax year that is not compensated by insurance or otherwise, subject to certain limitations. The new law temporarily limits the deduction for personal casualty and theft losses to losses incurred in a federally-declared disaster.

Miscellaneous itemized deductions: The deduction of job expenses and certain miscellaneous deductions (unreimbursed employee expenses, tax preparation fees, investment advisory fees, safety deposit box fees, etc.) in the aggregate which is greater than two percent of adjusted gross income has been eliminated.

Other changes to the tax law include the following deductions/credits/taxes:

Deductions that have been eliminated are: the alimony deduction (effective 1/1/19); moving expenses deduction (applicable to active duty military only); and tuition and fees deduction.

The Child Tax Credit has been modified by increasing the credit to $2,000 (from $1,000) per qualifying child and raises the modified adjusted gross income phase-out to $200,000 ($400,000 married filing joint) The new tax law now allows a $500 non-refundable tax credit for dependents who do not qualify for the child tax credit, as well as non-children dependents.

Education credits have been expanded to include distributions from 529 Plans for primary education (grades kindergarten through high school). The maximum amount of distribution allowed is $10,000 per year per student.

The Alternative Minimum Tax, a parallel tax system to the regular tax system, has been modified by increasing exemption amounts for individuals from $54,300 to $70,300 and $84,500 to $109,400 married filing jointly.

The Affordable Care Act Individual Mandate has been modified by eliminating the penalty for not having health insurance, effective January 1, 2019.

If you have any further questions and/or concerns about the new tax law, please consult your tax professional or call the Internal Revenue Service at 800-829-1040.

For more information contact:

Ron Friedman, CPA

914.830.4369